Governments generate revenue from income taxes. They are used to pay for government obligations, fund public services, and supply goods to residents.

Who is taxed on their personal income in Romania?

Romanian citizens domiciled in Romania are regarded as Romanian tax residents and are taxed on their worldwide income (except paychecks earned abroad for work performed abroad, which is tax exempt) unless they demonstrate, through tax residence documents, that they are eligible as tax residents of a state with which Romania has a double tax treaty (DTT). Some of the countries that signed DTTs with Romania are:

- Albania, Armenia, Algeria, Australia, Azerbaijan, Austria, Belgium, Belarus, Bangladesh, Bulgaria, Bosnia and Herzegovina, Canada, China, Cyprus, Croatia, Czech Republic, Denmark, Serbia, South Africa, Slovenia, Spain, Sudan, Sri Lanka, Switzerland, Sweden, Syria, Tajikistan, Tunisia, Thailand, Turkey, Turkmenistan, UK, the UAE, United Kingdom, the USA.

Romanian citizens domiciled in Romania who demonstrate tax residency status in a state that does not have a DTT agreement with Romania remain taxable in Romania on their worldwide income for the calendar year in which the change of residence occurs, as well as the next three calendar years.

Romanian nationals who are not domiciled in Romania, as well as foreign people, are taxed in Romania only on income earned in Romania, until they become Romanian tax residents, in which case they are taxed on their worldwide income. Non-resident individuals are taxed on their worldwide income beginning on the date they officially become tax residents in Romania (while adhering to the requirements of the DTTs).

Personal Tax Income

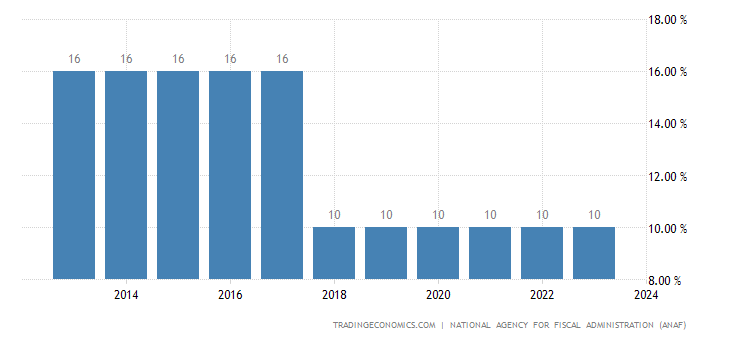

Personal income tax (PIT) is normally levied at a fixed rate of 10%. There are several exceptions to this rule, for example, the tax rate on dividends, the tax rate on income from the transfer of immovable property and the tax rate on income from gambling operations vary depending on income level.

The PIT Rate in Romania is set at 10 percent.

source: National Agency for Fiscal Administration (ANAF)

Social Contributions

Employers must deduct tax and social security contributions from the salaries of their staff and report them to the national tax authority by the 25th day of the month following the one for which such salary income is paid. Here are the general social contributions:

- Employers:

Employer pension insurance contribution: 4% for specific working circumstances or 8% for exceptional working conditions; no employer pension insurance payment for typical working conditions.

Contribution to social security: 2.25%.

- As established by legislation, several exclusions apply in the construction sector.

- Employees:

Pension insurance contribution: 25%.

Health insurance contribution: 10%.

- The gross income from dependent activities is the monthly assessment base.

Social contribution responsibilities are determined in accordance with EU social security coordination regulations and the provisions of the social security agreements, which Romania signed.

Conclusion

It is necessary to know the taxes that are imposed on your personal income in order to compute and evaluate your monthly financial situation.

source: PwC, Trading Economics